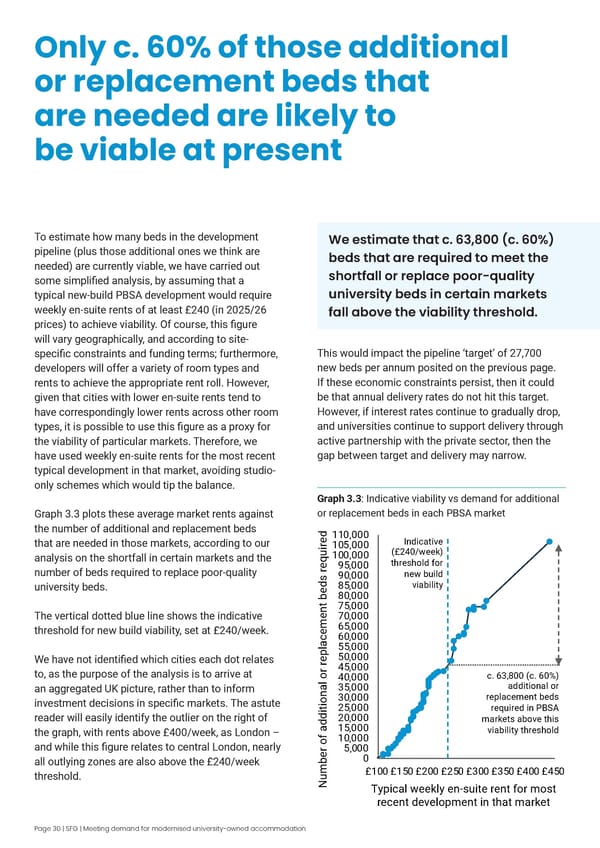

Only c. 60% of those additional or replacement beds that are needed are likely to be viable at present To estimate how many beds in the development pipeline (plus those additional ones we think are needed) are currently viable, we have carried out some simplified analysis, by assuming that a typical new-build PBSA development would require weekly en-suite rents of at least £240 (in 2025/26 prices) to achieve viability. Of course, this figure will vary geographically, and according to site- specific constraints and funding terms; furthermore, developers will offer a variety of room types and rents to achieve the appropriate rent roll. However, given that cities with lower en-suite rents tend to have correspondingly lower rents across other room types, it is possible to use this figure as a proxy for the viability of particular markets. Therefore, we have used weekly en-suite rents for the most recent typical development in that market, avoiding studio- only schemes which would tip the balance. Graph 3.3 plots these average market rents against the number of additional and replacement beds that are needed in those markets, according to our analysis on the shortfall in certain markets and the number of beds required to replace poor-quality university beds. The vertical dotted blue line shows the indicative threshold for new build viability, set at £240/week. We have not identified which cities each dot relates to, as the purpose of the analysis is to arrive at an aggregated UK picture, rather than to inform investment decisions in specific markets. The astute reader will easily identify the outlier on the right of the graph, with rents above £400/week, as London – and while this figure relates to central London, nearly all outlying zones are also above the £240/week threshold. We estimate that c. 63,800 (c. 60%) beds that are required to meet the shortfall or replace poor-quality university beds in certain markets fall above the viability threshold. This would impact the pipeline ‘target’ of 27,700 new beds per annum posited on the previous page. If these economic constraints persist, then it could be that annual delivery rates do not hit this target. However, if interest rates continue to gradually drop, and universities continue to support delivery through active partnership with the private sector, then the gap between target and delivery may narrow. Graph 3.3 : Indicative viability vs demand for additional or replacement beds in each PBSA market 0 5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000 45,000 50,000 55,000 60,000 65,000 70,000 75,000 80,000 85,000 90,000 95,000 100,000 105,000 110,000 £100 £150 £200 £250 £300 £350 £400 £450 Number of additional or replacement beds required Typical weekly en-suite rent for most recent development in that market c. 63,800 (c. 60%) additional or replacement beds required in PBSA markets above this viability threshold Indicative (£240/week) threshold for new build viability Page 30 | SFG | Meeting demand for modernised university-owned accommodation

Meeting demand for modernised university accommodation Page 31 Page 33

Meeting demand for modernised university accommodation Page 31 Page 33