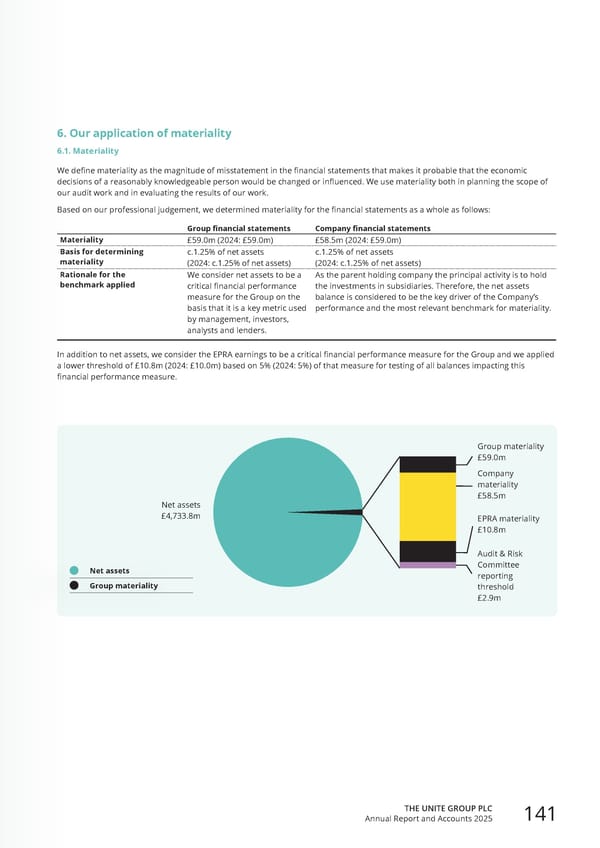

6. Our application of materiality 6.1. Materiality We define materiality as the magnitude of misstatement in the financial statements that makes it probable that the economic decisions of a reasonably knowledgeable person would be changed or influenced. We use materiality both in planning the scope of our audit work and in evaluating the results of our work. Based on our professional judgement, we determined materiality for the financial statements as a whole as follows: Group financial statements Company financial statements Materiality £59.0m (2024: £59.0m) £58.5m (2024: £59.0m) Basis for determining materiality c.1.25% of net assets (2024: c.1.25% of net assets) c.1.25% of net assets (2024: c.1.25% of net assets) Rationale for the benchmark applied We consider net assets to be a critical financial performance measure for the Group on the basis that it is a key metric used by management, investors, analysts and lenders. As the parent holding company the principal activity is to hold the investments in subsidiaries. Therefore, the net assets balance is considered to be the key driver of the Company’s performance and the most relevant benchmark for materiality. In addition to net assets, we consider the EPRA earnings to be a critical financial performance measure for the Group and we applied a lower threshold of £10.8m (2024: £10.0m) based on 5% (2024: 5%) of that measure for testing of all balances impacting this financial performance measure. Net assets Group materiality Group materiality £59.0m Net assets £4,733.8m Company materiality £58.5m Audit & Risk Committee reporting threshold £2.9m EPRA materiality £10.8m THE UNITE GROUP PLC Annual Report and Accounts 2025 141

Home for Success: Unite Students Annual Report 2025 Page 142 Page 144

Home for Success: Unite Students Annual Report 2025 Page 142 Page 144