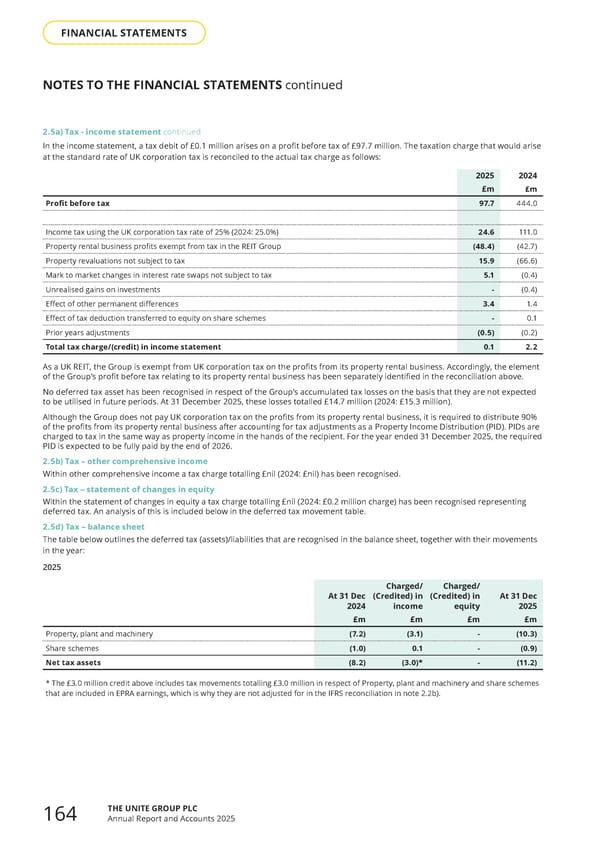

2.5a) Tax - income statement continued In the income statement, a tax debit of £0.1 million arises on a profit before tax of £97.7 million. The taxation charge that would arise at the standard rate of UK corporation tax is reconciled to the actual tax charge as follows: 2025 £m Profit before tax 97.7 Income tax using the UK corporation tax rate of 25% (2024: 25.0%) 24.6 Property rental business profits exempt from tax in the REIT Group (48.4) Property revaluations not subject to tax 15.9 Mark to market changes in interest rate swaps not subject to tax 5.1 Unrealised gains on investments - Effect of other permanent differences 3.4 Effect of tax deduction transferred to equity on share schemes - Prior years adjustments (0.5) Total tax charge/(credit) in income statement 0.1 As a UK REIT, the Group is exempt from UK corporation tax on the profits from its property rental business. Accordingly, the element of the Group’s profit before tax relating to its property rental business has been separately identified in the reconciliation above. No deferred tax asset has been recognised in respect of the Group’s accumulated tax losses on the basis that they are not expected to be utilised in future periods. At 31 December 2025, these losses totalled £14.7 million (2024: £15.3 million). Although the Group does not pay UK corporation tax on the profits from its property rental business, it is required to distribute 90% of the profits from its property rental business after accounting for tax adjustments as a Property Income Distribution (PID). PIDs are charged to tax in the same way as property income in the hands of the recipient. For the year ended 31 December 2025, the required PID is expected to be fully paid by the end of 2026. 2.5b) Tax – other comprehensive income Within other comprehensive income a tax charge totalling £nil (2024: £nil) has been recognised. 2.5c) Tax – statement of changes in equity Within the statement of changes in equity a tax charge totalling £nil (2024: £0.2 million charge) has been recognised representing deferred tax. An analysis of this is included below in the deferred tax movement table. 2.5d) Tax – balance sheet The table below outlines the deferred tax (assets)/liabilities that are recognised in the balance sheet, together with their movements in the year: 2025 At 31 Dec 2024 Charged/ (Credited) in income Charged/ (Credited) in equity At 31 Dec 2025 £m £m £m £m Property, plant and machinery (7.2) (3.1) - (10.3) Share schemes (1.0) 0.1 - (0.9) Net tax assets (8.2) (3.0)* - (11.2) * The £3.0 million credit above includes tax movements totalling £3.0 million in respect of Property, plant and machinery and share schemes that are included in EPRA earnings, which is why they are not adjusted for in the IFRS reconciliation in note 2.2b). NOTES TO THE FINANCIAL STATEMENTS continued 2024 £m 444.0 111.0 (42.7) (66.6) (0.4) (0.4) 1.4 0.1 (0.2) 2.2 THE UNITE GROUP PLC Annual Report and Accounts 2025 164 FINANCIAL STATEMENTS

Home for Success: Unite Students Annual Report 2025 Page 165 Page 167

Home for Success: Unite Students Annual Report 2025 Page 165 Page 167