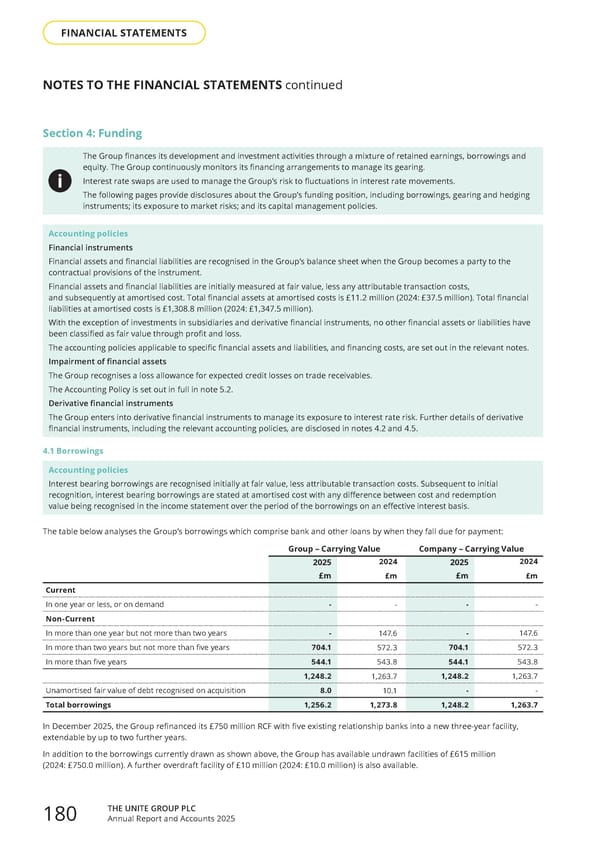

Section 4: Funding The Group finances its development and investment activities through a mixture of retained earnings, borrowings and equity. The Group continuously monitors its financing arrangements to manage its gearing. Interest rate swaps are used to manage the Group’s risk to fluctuations in interest rate movements. The following pages provide disclosures about the Group’s funding position, including borrowings, gearing and hedging instruments; its exposure to market risks; and its capital management policies. Accounting policies Financial instruments Financial assets and financial liabilities are recognised in the Group’s balance sheet when the Group becomes a party to the contractual provisions of the instrument. Financial assets and financial liabilities are initially measured at fair value, less any attributable transaction costs, and subsequently at amortised cost. Total financial assets at amortised costs is £11.2 million (2024: £37.5 million). Total financial liabilities at amortised costs is £1,308.8 million (2024: £1,347.5 million). With the exception of investments in subsidiaries and derivative financial instruments, no other financial assets or liabilities have been classified as fair value through profit and loss. The accounting policies applicable to specific financial assets and liabilities, and financing costs, are set out in the relevant notes. Impairment of financial assets The Group recognises a loss allowance for expected credit losses on trade receivables. The Accounting Policy is set out in full in note 5.2. Derivative financial instruments The Group enters into derivative financial instruments to manage its exposure to interest rate risk. Further details of derivative financial instruments, including the relevant accounting policies, are disclosed in notes 4.2 and 4.5. 4.1 Borrowings Accounting policies Interest bearing borrowings are recognised initially at fair value, less attributable transaction costs. Subsequent to initial recognition, interest bearing borrowings are stated at amortised cost with any difference between cost and redemption value being recognised in the income statement over the period of the borrowings on an effective interest basis. The table below analyses the Group’s borrowings which comprise bank and other loans by when they fall due for payment: Group – Carrying Value Company – Carrying Value 2025 2025 £m £m Current In one year or less, or on demand - - Non-Current In more than one year but not more than two years - - In more than two years but not more than five years 704.1 704.1 In more than five years 544.1 544.1 1,248.2 1,248.2 Unamortised fair value of debt recognised on acquisition 8.0 - Total borrowings 1,256.2 1,248.2 In December 2025, the Group refinanced its £750 million RCF with five existing relationship banks into a new three-year facility, extendable by up to two further years. In addition to the borrowings currently drawn as shown above, the Group has available undrawn facilities of £615 million (2024: £750.0 million). A further overdraft facility of £10 million (2024: £10.0 million) is also available. NOTES TO THE FINANCIAL STATEMENTS continued 2024 £m - 147.6 572.3 543.8 1,263.7 10.1 1,273.8 2024 £m - 147.6 572.3 543.8 1,263.7 - 1,263.7 THE UNITE GROUP PLC Annual Report and Accounts 2025 180 FINANCIAL STATEMENTS

Home for Success: Unite Students Annual Report 2025 Page 181 Page 183

Home for Success: Unite Students Annual Report 2025 Page 181 Page 183