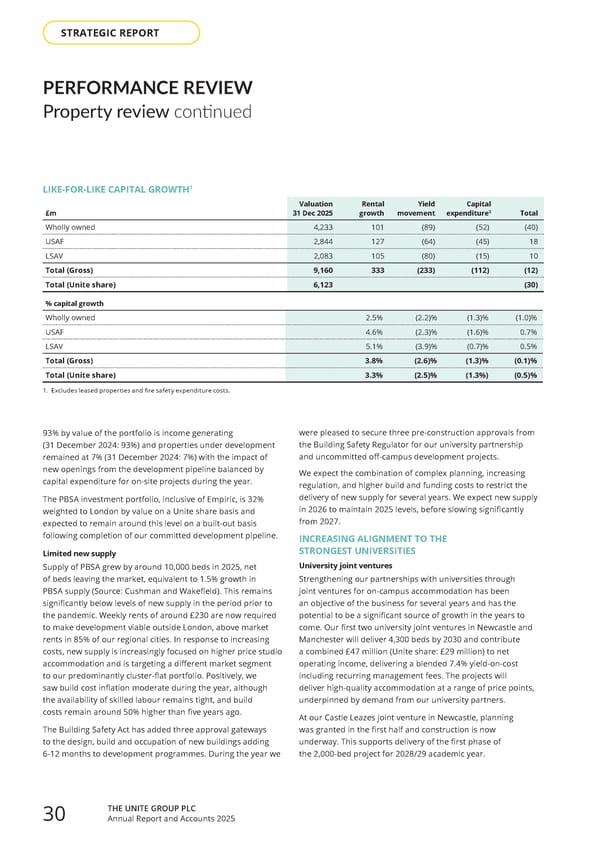

93% by value of the portfolio is income generating (31 December 2024: 93%) and properties under development remained at 7% (31 December 2024: 7%) with the impact of new openings from the development pipeline balanced by capital expenditure for on-site projects during the year. The PBSA investment portfolio, inclusive of Empiric, is 32% weighted to London by value on a Unite share basis and expected to remain around this level on a built-out basis following completion of our committed development pipeline. Limited new supply Supply of PBSA grew by around 10,000 beds in 2025, net of beds leaving the market, equivalent to 1.5% growth in PBSA supply (Source: Cushman and Wakefield). This remains significantly below levels of new supply in the period prior to the pandemic. Weekly rents of around £230 are now required to make development viable outside London, above market rents in 85% of our regional cities. In response to increasing costs, new supply is increasingly focused on higher price studio accommodation and is targeting a different market segment to our predominantly cluster-flat portfolio. Positively, we saw build cost inflation moderate during the year, although the availability of skilled labour remains tight, and build costs remain around 50% higher than five years ago. The Building Safety Act has added three approval gateways to the design, build and occupation of new buildings adding 6-12 months to development programmes. During the year we were pleased to secure three pre-construction approvals from the Building Safety Regulator for our university partnership and uncommitted off-campus development projects. We expect the combination of complex planning, increasing regulation, and higher build and funding costs to restrict the delivery of new supply for several years. We expect new supply in 2026 to maintain 2025 levels, before slowing significantly from 2027. INCREASING ALIGNMENT TO THE STRONGEST UNIVERSITIES University joint ventures Strengthening our partnerships with universities through joint ventures for on-campus accommodation has been an objective of the business for several years and has the potential to be a significant source of growth in the years to come. Our first two university joint ventures in Newcastle and Manchester will deliver 4,300 beds by 2030 and contribute a combined £47 million (Unite share: £29 million) to net operating income, delivering a blended 7.4% yield-on-cost including recurring management fees. The projects will deliver high-quality accommodation at a range of price points, underpinned by demand from our university partners. At our Castle Leazes joint venture in Newcastle, planning was granted in the first half and construction is now underway. This supports delivery of the first phase of the 2,000-bed project for 2028/29 academic year. PERFORMANCE REVIEW Property review continued LIKE-FOR-LIKE CAPITAL GROWTH 1 £m Valuation 31 Dec 2025 Rental growth Yield movement Capital expenditure 3 Total Wholly owned 4,233 101 (89) (52) (40) USAF 2,844 127 (64) (45) 18 LSAV 2,083 105 (80) (15) 10 Total (Gross) 9,160 333 (233) (112) (12) Total (Unite share) 6,123 (30) % capital growth Wholly owned 2.5% (2.2)% (1.3)% (1.0)% USAF 4.6% (2.3)% (1.6)% 0.7% LSAV 5.1% (3.9)% (0.7)% 0.5% Total (Gross) 3.8% (2.6)% (1.3)% (0.1)% Total (Unite share) 3.3% (2.5)% (1.3%) (0.5)% 1 . Excludes leased properties and fire safety expenditure costs. THE UNITE GROUP PLC Annual Report and Accounts 2025 30 STRATEGIC REPORT

Home for Success: Unite Students Annual Report 2025 Page 31 Page 33

Home for Success: Unite Students Annual Report 2025 Page 31 Page 33