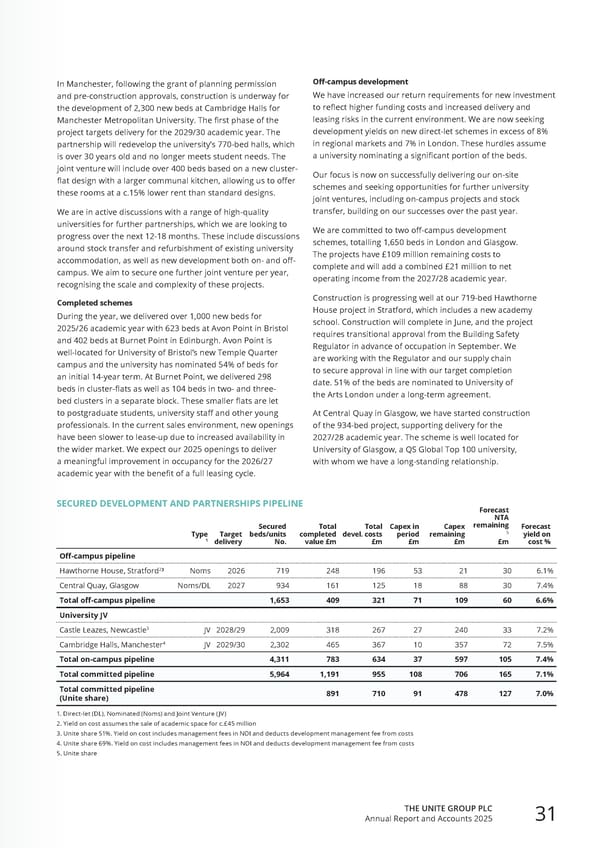

In Manchester, following the grant of planning permission and pre-construction approvals, construction is underway for the development of 2,300 new beds at Cambridge Halls for Manchester Metropolitan University. The first phase of the project targets delivery for the 2029/30 academic year. The partnership will redevelop the university’s 770-bed halls, which is over 30 years old and no longer meets student needs. The joint venture will include over 400 beds based on a new cluster- flat design with a larger communal kitchen, allowing us to offer these rooms at a c.15% lower rent than standard designs. We are in active discussions with a range of high-quality universities for further partnerships, which we are looking to progress over the next 12-18 months. These include discussions around stock transfer and refurbishment of existing university accommodation, as well as new development both on- and off- campus. We aim to secure one further joint venture per year, recognising the scale and complexity of these projects. Completed schemes During the year, we delivered over 1,000 new beds for 2025/26 academic year with 623 beds at Avon Point in Bristol and 402 beds at Burnet Point in Edinburgh. Avon Point is well-located for University of Bristol’s new Temple Quarter campus and the university has nominated 54% of beds for an initial 14-year term. At Burnet Point, we delivered 298 beds in cluster-flats as well as 104 beds in two- and three- bed clusters in a separate block. These smaller flats are let to postgraduate students, university staff and other young professionals. In the current sales environment, new openings have been slower to lease-up due to increased availability in the wider market. We expect our 2025 openings to deliver a meaningful improvement in occupancy for the 2026/27 academic year with the benefit of a full leasing cycle. Off-campus development We have increased our return requirements for new investment to reflect higher funding costs and increased delivery and leasing risks in the current environment. We are now seeking development yields on new direct-let schemes in excess of 8% in regional markets and 7% in London. These hurdles assume a university nominating a significant portion of the beds. Our focus is now on successfully delivering our on-site schemes and seeking opportunities for further university joint ventures, including on-campus projects and stock transfer, building on our successes over the past year. We are committed to two off-campus development schemes, totalling 1,650 beds in London and Glasgow. The projects have £109 million remaining costs to complete and will add a combined £21 million to net operating income from the 2027/28 academic year. Construction is progressing well at our 719-bed Hawthorne House project in Stratford, which includes a new academy school. Construction will complete in June, and the project requires transitional approval from the Building Safety Regulator in advance of occupation in September. We are working with the Regulator and our supply chain to secure approval in line with our target completion date. 51% of the beds are nominated to University of the Arts London under a long-term agreement. At Central Quay in Glasgow, we have started construction of the 934-bed project, supporting delivery for the 2027/28 academic year. The scheme is well located for University of Glasgow, a QS Global Top 100 university, with whom we have a long-standing relationship. SECURED DEVELOPMENT AND PARTNERSHIPS PIPELINE Type 1 Target delivery Secured beds/units No. Total completed value £m Total devel. costs £m Capex in period £m Capex remaining £m Forecast NTA remaining 5 £m Forecast yield on cost % Off-campus pipeline Hawthorne House, Stratford 2 ³ Noms 2026 719 248 196 53 21 30 6.1% Central Quay, Glasgow Noms/DL 2027 934 161 125 18 88 30 7.4% Total off-campus pipeline 1,653 409 321 71 109 60 6.6% University JV Castle Leazes, Newcastle 3 JV 2028/29 2,009 318 267 27 240 33 7.2% Cambridge Halls, Manchester 4 JV 2029/30 2,302 465 367 10 357 72 7.5% Total on-campus pipeline 4,311 783 634 37 597 105 7.4% Total committed pipeline 5,964 1,191 955 108 706 165 7.1% Total committed pipeline (Unite share) 891 710 91 478 127 7.0% 1. Direct-let (DL), Nominated (Noms) and Joint Venture ( JV) 2. Yield on cost assumes the sale of academic space for c.£45 million 3. Unite share 51%. Yield on cost includes management fees in NOI and deducts development management fee from costs 4. Unite share 69%. Yield on cost includes management fees in NOI and deducts development management fee from costs 5. Unite share THE UNITE GROUP PLC Annual Report and Accounts 2025 31

Home for Success: Unite Students Annual Report 2025 Page 32 Page 34

Home for Success: Unite Students Annual Report 2025 Page 32 Page 34