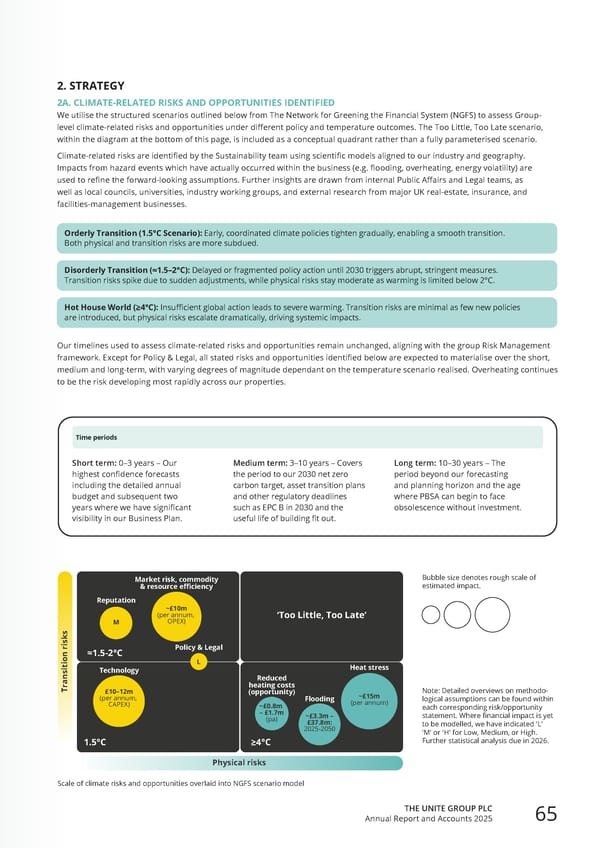

2. STRATEGY 2A. CLIMATE-RELATED RISKS AND OPPORTUNITIES IDENTIFIED We utilise the structured scenarios outlined below from The Network for Greening the Financial System (NGFS) to assess Group- level climate-related risks and opportunities under different policy and temperature outcomes. The Too Little, Too Late scenario, within the diagram at the bottom of this page, is included as a conceptual quadrant rather than a fully parameterised scenario. Climate - related risks are identified by the Sustainability team using scientific models aligned to our industry and geography. Impacts from hazard events which have actually occurred within the business (e.g. flooding, overheating, energy volatility) are used to refine the forward - looking assumptions. Further insights are drawn from internal Public Affairs and Legal teams, as well as local councils, universities, industry working groups, and external research from major UK real - estate, insurance, and facilities - management businesses. Orderly Transition (1.5°C Scenario): Early, coordinated climate policies tighten gradually, enabling a smooth transition. Both physical and transition risks are more subdued. Disorderly Transition (≈1.5–2°C): Delayed or fragmented policy action until 2030 triggers abrupt, stringent measures. Transition risks spike due to sudden adjustments, while physical risks stay moderate as warming is limited below 2°C. Hot House World (≥4°C): Insufficient global action leads to severe warming. Transition risks are minimal as few new policies are introduced, but physical risks escalate dramatically, driving systemic impacts. Our timelines used to assess climate-related risks and opportunities remain unchanged, aligning with the group Risk Management framework. Except for Policy & Legal, all stated risks and opportunities identified below are expected to materialise over the short, medium and long-term, with varying degrees of magnitude dependant on the temperature scenario realised. Overheating continues to be the risk developing most rapidly across our properties. Scale of climate risks and opportunities overlaid into NGFS scenario model Short term: 0–3 years – Our highest confidence forecasts including the detailed annual budget and subsequent two years where we have significant visibility in our Business Plan. Medium term: 3–10 years – Covers the period to our 2030 net zero carbon target, asset transition plans and other regulatory deadlines such as EPC B in 2030 and the useful life of building fit out. Long term: 10–30 years – The period beyond our forecasting and planning horizon and the age where PBSA can begin to face obsolescence without investment. Time periods ~£15m (per annum) ~£3.3m – £37.8m: 2025-2050 Flooding Heat stress Reduced heating costs (opportunity) Market risk, commodity & resource efficiency Reputation M L ~£10m (per annum, OPEX) Transition risks Physical risks £10–12m (per annum, CAPEX) Technology Policy & Legal ≈1.5-2°C 1.5°C ≥4°C ‘Too Little, Too Late’ ~£0.8m – £1.7m (pa) Note: Detailed overviews on methodo- logical assumptions can be found within each corresponding risk/opportunity statement. Where financial impact is yet to be modelled, we have indicated 'L' 'M' or 'H' for Low, Medium, or High. Further statistical analysis due in 2026. Bubble size denotes rough scale of estimated impact. THE UNITE GROUP PLC Annual Report and Accounts 2025 65

Home for Success: Unite Students Annual Report 2025 Page 66 Page 68

Home for Success: Unite Students Annual Report 2025 Page 66 Page 68