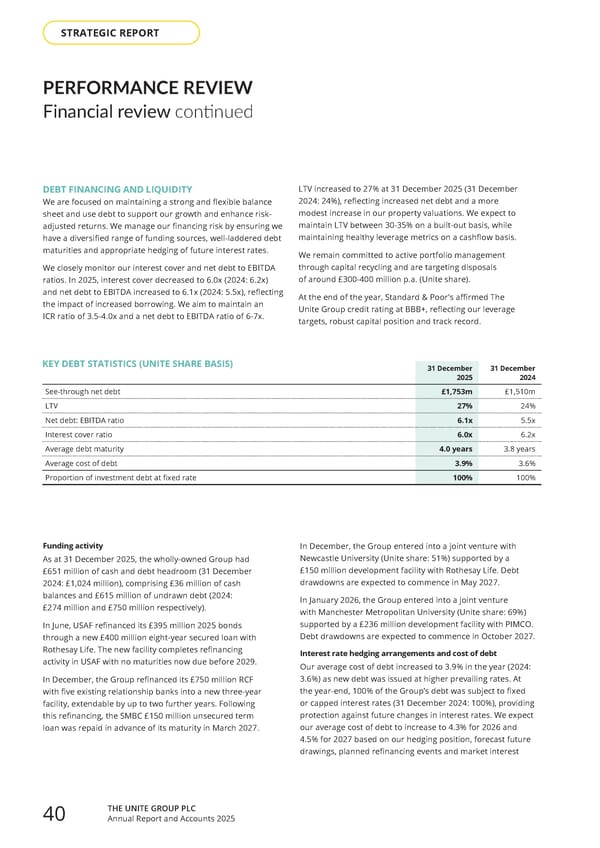

PERFORMANCE REVIEW Financial review continued DEBT FINANCING AND LIQUIDITY We are focused on maintaining a strong and flexible balance sheet and use debt to support our growth and enhance risk- adjusted returns. We manage our financing risk by ensuring we have a diversified range of funding sources, well-laddered debt maturities and appropriate hedging of future interest rates. We closely monitor our interest cover and net debt to EBITDA ratios. In 2025, interest cover decreased to 6.0x (2024: 6.2x) and net debt to EBITDA increased to 6.1x (2024: 5.5x), reflecting the impact of increased borrowing. We aim to maintain an ICR ratio of 3.5-4.0x and a net debt to EBITDA ratio of 6-7x. KEY DEBT STATISTICS (UNITE SHARE BASIS) 31 December 2025 31 December 2024 See-through net debt £1,753m £1,510m LTV 27% 24% Net debt: EBITDA ratio 6.1x 5.5x Interest cover ratio 6.0x 6.2x Average debt maturity 4.0 years 3.8 years Average cost of debt 3.9% 3.6% Proportion of investment debt at fixed rate 100% 100% Funding activity As at 31 December 2025, the wholly-owned Group had £651 million of cash and debt headroom (31 December 2024: £1,024 million), comprising £36 million of cash balances and £615 million of undrawn debt (2024: £274 million and £750 million respectively). In June, USAF refinanced its £395 million 2025 bonds through a new £400 million eight-year secured loan with Rothesay Life. The new facility completes refinancing activity in USAF with no maturities now due before 2029. In December, the Group refinanced its £750 million RCF with five existing relationship banks into a new three-year facility, extendable by up to two further years. Following this refinancing, the SMBC £150 million unsecured term loan was repaid in advance of its maturity in March 2027. In December, the Group entered into a joint venture with Newcastle University (Unite share: 51%) supported by a £150 million development facility with Rothesay Life. Debt drawdowns are expected to commence in May 2027. In January 2026, the Group entered into a joint venture with Manchester Metropolitan University (Unite share: 69%) supported by a £236 million development facility with PIMCO. Debt drawdowns are expected to commence in October 2027. Interest rate hedging arrangements and cost of debt Our average cost of debt increased to 3.9% in the year (2024: 3.6%) as new debt was issued at higher prevailing rates. At the year-end, 100% of the Group’s debt was subject to fixed or capped interest rates (31 December 2024: 100%), providing protection against future changes in interest rates. We expect our average cost of debt to increase to 4.3% for 2026 and 4.5% for 2027 based on our hedging position, forecast future drawings, planned refinancing events and market interest LTV increased to 27% at 31 December 2025 (31 December 2024: 24%), reflecting increased net debt and a more modest increase in our property valuations. We expect to maintain LTV between 30-35% on a built-out basis, while maintaining healthy leverage metrics on a cashflow basis. We remain committed to active portfolio management through capital recycling and are targeting disposals of around £300-400 million p.a. (Unite share). At the end of the year, Standard & Poor's affirmed The Unite Group credit rating at BBB+, reflecting our leverage targets, robust capital position and track record. THE UNITE GROUP PLC Annual Report and Accounts 2025 40 STRATEGIC REPORT

Home for Success: Unite Students Annual Report 2025 Page 41 Page 43

Home for Success: Unite Students Annual Report 2025 Page 41 Page 43