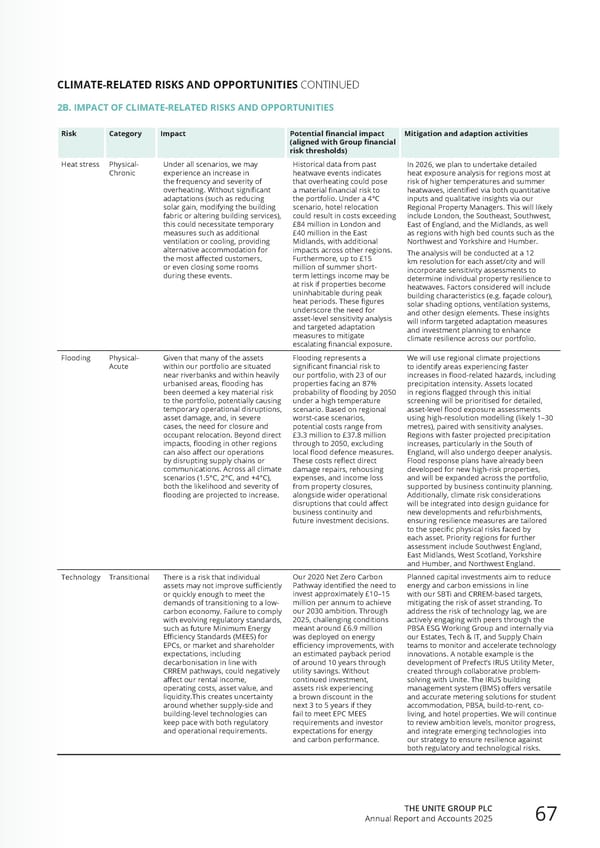

CLIMATE-RELATED RISKS AND OPPORTUNITIES CONTINUED Risk Category Impact Potential financial impact (aligned with Group financial risk thresholds) Mitigation and adaption activities Heat stress Physical- Chronic Under all scenarios, we may experience an increase in the frequency and severity of overheating. Without significant adaptations (such as reducing solar gain, modifying the building fabric or altering building services), this could necessitate temporary measures such as additional ventilation or cooling, providing alternative accommodation for the most affected customers, or even closing some rooms during these events. Historical data from past heatwave events indicates that overheating could pose a material financial risk to the portfolio. Under a 4°C scenario, hotel relocation could result in costs exceeding £84 million in London and £40 million in the East Midlands, with additional impacts across other regions. Furthermore, up to £15 million of summer short- term lettings income may be at risk if properties become uninhabitable during peak heat periods. These figures underscore the need for asset-level sensitivity analysis and targeted adaptation measures to mitigate escalating financial exposure. In 2026, we plan to undertake detailed heat exposure analysis for regions most at risk of higher temperatures and summer heatwaves, identified via both quantitative inputs and qualitative insights via our Regional Property Managers. This will likely include London, the Southeast, Southwest, East of England, and the Midlands, as well as regions with high bed counts such as the Northwest and Yorkshire and Humber. The analysis will be conducted at a 12 km resolution for each asset/city and will incorporate sensitivity assessments to determine individual property resilience to heatwaves. Factors considered will include building characteristics (e.g. façade colour), solar shading options, ventilation systems, and other design elements. These insights will inform targeted adaptation measures and investment planning to enhance climate resilience across our portfolio. Flooding Physical- Acute Given that many of the assets within our portfolio are situated near riverbanks and within heavily urbanised areas, flooding has been deemed a key material risk to the portfolio, potentially causing temporary operational disruptions, asset damage, and, in severe cases, the need for closure and occupant relocation. Beyond direct impacts, flooding in other regions can also affect our operations by disrupting supply chains or communications. Across all climate scenarios (1.5°C, 2°C, and +4°C), both the likelihood and severity of flooding are projected to increase. Flooding represents a significant financial risk to our portfolio, with 23 of our properties facing an 87% probability of flooding by 2050 under a high temperature scenario. Based on regional worst-case scenarios, potential costs range from £3.3 million to £37.8 million through to 2050, excluding local flood defence measures. These costs reflect direct damage repairs, rehousing expenses, and income loss from property closures, alongside wider operational disruptions that could affect business continuity and future investment decisions. We will use regional climate projections to identify areas experiencing faster increases in flood-related hazards, including precipitation intensity. Assets located in regions flagged through this initial screening will be prioritised for detailed, asset-level flood exposure assessments using high-resolution modelling (likely 1–30 metres), paired with sensitivity analyses. Regions with faster projected precipitation increases, particularly in the South of England, will also undergo deeper analysis. Flood response plans have already been developed for new high-risk properties, and will be expanded across the portfolio, supported by business continuity planning. Additionally, climate risk considerations will be integrated into design guidance for new developments and refurbishments, ensuring resilience measures are tailored to the specific physical risks faced by each asset. Priority regions for further assessment include Southwest England, East Midlands, West Scotland, Yorkshire and Humber, and Northwest England. Technology Transitional There is a risk that individual assets may not improve sufficiently or quickly enough to meet the demands of transitioning to a low- carbon economy. Failure to comply with evolving regulatory standards, such as future Minimum Energy Efficiency Standards (MEES) for EPCs, or market and shareholder expectations, including decarbonisation in line with CRREM pathways, could negatively affect our rental income, operating costs, asset value, and liquidity.This creates uncertainty around whether supply-side and building-level technologies can keep pace with both regulatory and operational requirements. Our 2020 Net Zero Carbon Pathway identified the need to invest approximately £10–15 million per annum to achieve our 2030 ambition. Through 2025, challenging conditions meant around £6.9 million was deployed on energy efficiency improvements, with an estimated payback period of around 10 years through utility savings. Without continued investment, assets risk experiencing a brown discount in the next 3 to 5 years if they fail to meet EPC MEES requirements and investor expectations for energy and carbon performance. Planned capital investments aim to reduce energy and carbon emissions in line with our SBTi and CRREM-based targets, mitigating the risk of asset stranding. To address the risk of technology lag, we are actively engaging with peers through the PBSA ESG Working Group and internally via our Estates, Tech & IT, and Supply Chain teams to monitor and accelerate technology innovations. A notable example is the development of Prefect’s IRUS Utility Meter, created through collaborative problem- solving with Unite. The IRUS building management system (BMS) offers versatile and accurate metering solutions for student accommodation, PBSA, build-to-rent, co- living, and hotel properties. We will continue to review ambition levels, monitor progress, and integrate emerging technologies into our strategy to ensure resilience against both regulatory and technological risks. 2B. IMPACT OF CLIMATE-RELATED RISKS AND OPPORTUNITIES THE UNITE GROUP PLC Annual Report and Accounts 2025 67

Home for Success: Unite Students Annual Report 2025 Page 68 Page 70

Home for Success: Unite Students Annual Report 2025 Page 68 Page 70